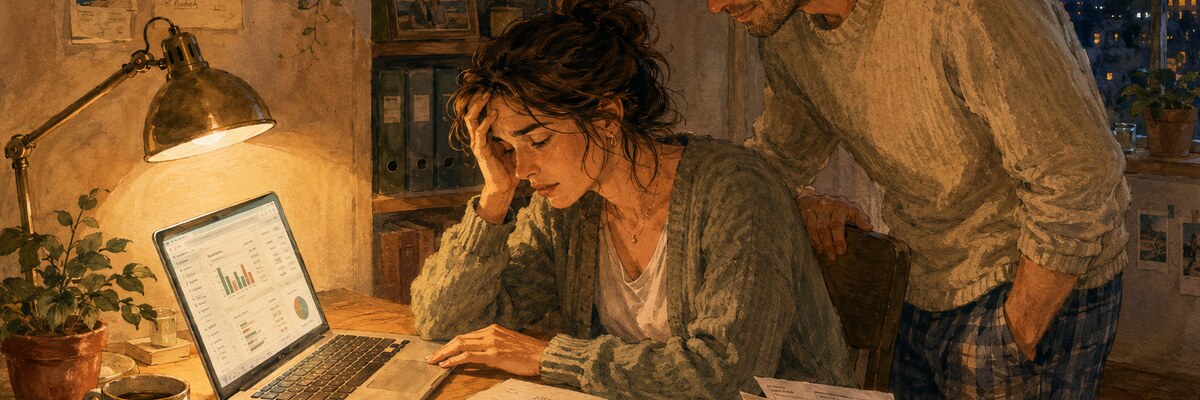

She earns $150,000. She refreshes her banking app at red lights and feels her stomach drop every time. He earns $40,000. He bought concert tickets last week without checking the balance and slept fine. They've been together six years, and they fight about money once a week — but only one of them has actually been doing the math.

This isn't a story about bad budgeting. Both of these people are responsible. The savings account is healthy. There is, by any reasonable accounting, enough.

What they have is money dysmorphia in relationships: a quiet, increasingly common gap between what you have and what you feel you have, and the way that gap warps every joint financial decision when two partners' versions of "the truth" don't match. The numbers are knowable. The feelings, weirdly, are not.

If you've ever had a fight that started with "you spent how much on the coffee maker?" and ended somewhere completely different — somewhere about safety, control, the way one of you was raised, the year someone's parents nearly lost the house — this is the article for you. Money dysmorphia is the quiet engine under most of those fights, and once you can name it, you can stop arguing the spreadsheet and start having the actual conversation.

What Money Dysmorphia Actually Is

The term went mainstream in 2024, after Credit Karma published a survey that put a number on a feeling a lot of people had been carrying alone: roughly 43% of Gen Z and 41% of millennials reported feeling "behind" financially, regardless of what their bank statements said. The numbers got picked up by The Wall Street Journal, CNBC, and a wave of TikTok creators, and a name finally stuck.

It is, importantly, not a clinical diagnosis. There's no DSM entry for money dysmorphia, and any therapist will tell you so. What it is, instead, is a useful name for something that wasn't named before — the disconnect between objective financial reality and the subjective sense of "am I okay." Body dysmorphia is the closest analogue: the mirror shows one thing, the brain reports another, and the brain wins.

For our purposes — couples — what matters is this: the feeling does not require the facts to support it. You can have six months of expenses saved and still feel like you're one bad month from the wheels coming off. You can have credit card debt and feel comfortable because the minimum payment is automated. The math and the felt sense have decoupled, and once they do, no amount of spreadsheet evidence will reattach them.

Why It Hits Couples Harder Than Individuals

If you have money dysmorphia and you're single, you basically have a private problem. You feel broke, you act broke, the worst that happens is you skip a vacation you could have afforded. Annoying, but contained.

Inside a relationship, the dysmorphia stops being private. Your partner sees the same bank account you do — and reaches a different conclusion. Three things go wrong from there.

1. Every spending decision becomes a referendum on whose feelings are valid.

If you feel broke and your partner doesn't, then every $80 dinner becomes proof that they don't take your fear seriously. If you feel fine and your partner doesn't, then every cautious "we shouldn't" becomes proof that they don't trust the life you've built together. Same dollar, opposite weight.

2. The "winning" partner gets exhausted, and the "losing" partner gets resentful.

If one of you is consistently right about the numbers — the savings account really is fine, the rent really is affordable — they win every argument and lose every relationship. The other one is left feeling unheard and a little crazy, which is a particular kind of slow-burn damage no spreadsheet fixes.

3. Money becomes the only language you fight in.

This is the most insidious. Couples with money dysmorphia often have other things they're worried about — mismatched career trajectories, kids vs. no kids, one of you carrying more emotional labour at home — but money is the proxy. It's concrete. It has numbers. It feels arguable. So the fight that's really about not feeling cared for becomes, again, a fight about the coffee maker. We've written before about how conversations stop working mid-fight when the surface topic isn't the real one. Money dysmorphia is one of the most common reasons that happens — and in long-relationship couples who've quietly slipped into roommate marriage, money fights are sometimes the only fights left, because everything else has gone too quiet to argue about.

The Four Patterns We See in Couples

Money dysmorphia in relationships doesn't show up just one way. There are four common pairings, and the shape of your specific fight is usually determined by which one you're in.

One of you has the dysmorphia, the other doesn't. The non-dysmorphic partner keeps "winning" the math arguments and slowly losing patience. The dysmorphic partner keeps feeling overruled, which makes the fear bigger, not smaller.

What it sounds like: "We literally have $30,000 in savings, why are you stressed?" / "You don't get it, I just need to know the number isn't going down."

Both of you feel broke, both of you stay broke-feeling, neither of you spend on the relationship. You pile up money you'll never enjoy. Vacations get postponed indefinitely. The shared scarcity feels like teamwork, but it's quietly preventing you from building any of the joint memories that make money worth having.

What it sounds like: "We can't justify it." / "Maybe next year." / "Let's just stay home."

Reverse dysmorphia: both of you feel fine when the numbers say otherwise. You confirm each other's worldview. The credit card statement arrives, and you're both surprised — sincerely. This is the pairing where things are genuinely fine until they suddenly aren't, because nobody is the brake.

What it sounds like: "We deserve this." / "We can figure it out." / "It's just one weekend."

One of you feels broke; the other feels fine. The numbers actually support the worried partner — but the calm partner thinks the worried one is being dramatic, because they grew up seeing real money panic and this doesn't look like that. Both of you are responding to memory, not reality. Both of you are right inside your own frame, and neither of you is talking about the same year.

What it sounds like: "You're catastrophising." / "You're not taking this seriously."

If you read those four patterns and felt a flash of recognition, that's the patten. Notice that none of them is solved by being better at math.

How to Tell If You're the One With It

The hardest version of this is the partner who has money dysmorphia and doesn't realise. From the inside, the fear feels reasonable — proportional, careful, adult. The signature of dysmorphia, in our experience and the way the financial-therapy literature describes it, is not the worry itself. It's how the worry behaves when the situation changes.

Try this self-check: imagine your bank balance doubles tomorrow. No strings, no catch, just a higher number. Sit with the imagined version for a minute. Does the felt sense of "I'm broke" actually loosen, or does the worry just find a new ceiling — a bigger savings target, a new scenario, a fresh reason it still isn't enough?

Normal financial anxiety scales with the situation. Money dysmorphia stays the same shape regardless of the input. If you ran the thought experiment and the answer was "I'd just want $100k more," that's the tell.

Three other quiet markers, often pointed out by financial therapists:

- Compulsive checking. Refreshing the banking app multiple times a day, even when you know nothing has changed. This is the closest body-dysmorphia analogue: re-confirming the mirror.

- Joy gets pre-empted by the math. Good things — a raise, a paid-off card, a holiday — get a brief flash of relief, then almost immediately you're calculating what's still missing.

- Generosity feels physically harder than it should. A $40 birthday gift triggers an internal weighing process that's out of proportion to the amount.

None of these are character flaws. They're the predictable shape of a nervous system that learned, somewhere along the way, that the number on the screen is a stand-in for safety, and so the screen has to be checked.

How to Tell If They Have It

From the outside, it's harder. The worried partner often does the worrying privately, and the calm partner often only sees the spillover — the snap when you mention dinner out, the reflexive no to small spends. A few signals to watch for, gently:

- Their reaction to a financial positive — like a bonus or a refund — is measurably smaller than their reaction to a comparable financial negative.

- They have a target number they keep moving. Last year it was $20K. Now you've hit $20K and it's actually $40K. That's not a savings plan; that's the dysmorphia rearranging the goalposts.

- They reach for catastrophe vocabulary — "we'll be ruined," "we can't afford this" — for purchases that are objectively well within budget.

- They have a story from childhood that contains the word "almost." Almost lost the house. Almost couldn't pay tuition. Whatever the almost is, it tends to live in the body for a long time.

The Conversation That Needs to Happen (Not the Spreadsheet)

The mistake most couples make once they recognise money dysmorphia is to try to fix it with information. Look — see, here's what we have. Look at the chart. It doesn't work. Information was never the missing piece. The missing piece is permission to feel broke without being told you're wrong.

The conversation that does work has three parts, and it's worth doing on a calm Sunday with no decisions on the table — not in the middle of a fight about a $200 chair.

Part 1: Tell each other your earliest money memory.

Not your first job. The first time money meant something emotional in your house. Whose face. What was said. Whether the room got quieter or louder. This usually surfaces the original wiring — the year your dysmorphia, if you have it, started learning its job. We've found this exercise so consistently useful that it's the spiritual cousin of the structured conversation we built Heart to Heart for.

Part 2: Each of you names your "felt floor."

The number below which the dysmorphic partner cannot be reasoned with. The number that, if it stayed in a savings account untouched, would let the nervous system stand down. This isn't a budget — it's a safety reserve. The non-dysmorphic partner agrees to never argue against this number. The dysmorphic partner agrees that once it's intact, money above it is allowed to be spent without litigation.

Part 3: Set a money date, monthly, with a hard stop.

30 minutes, calendar-blocked, the same day every month. You look at the joint situation together. You're allowed to bring up worries; you're not allowed to ambush each other on a Wednesday at 9pm. The structure is the gift — it gives the dysmorphic partner a known time to bring fears, which paradoxically reduces how often the fears need to spill into ordinary days.

Money Dysmorphia vs. Actual Financial Anxiety: The Caveat

Everything we've said so far assumes the numbers are objectively fine. We have to be careful here, because they aren't always. If you're a household where rent went up 18% this year and groceries are quietly devouring the line item that used to be "fun," your worry isn't dysmorphia — it's accurate. Naming actual scarcity as "just dysmorphia" is the worst possible misuse of this article.

The clinical-ish line: dysmorphia is when the fear stays the same regardless of the math. Actual financial pressure is when the fear scales with the situation. If a raise would, in fact, change how you feel — that's not dysmorphia, that's reality, and the conversation you need is different (and possibly involves a third party who can help you map a real plan).

If you're not sure which one you're in, that itself is data. A financial therapist — yes, that's a real specialty now, separate from a financial advisor — is trained for exactly this distinction. The Financial Therapy Association maintains a directory; some couples therapists list it as a specialty. It is not the same as advice on whether to buy index funds.

A Quieter Version: Heart to Heart's Money Track

If reading the conversation above made you tense up — fair. The Part 1 question (your earliest money memory) is one of the harder ones to ask cold. We built Heart to Heart partly because conversations like this work better with structure: the question gets surfaced for you, the turn-taking is built in, and neither of you has to be the one to "bring it up."

It's the same intuition behind the four-pattern map above — the goal isn't to solve money dysmorphia in a single sitting. It's to make sure both of you are in the same conversation, looking at the same year. From there, the math gets a lot easier, because the math was never the problem.

Frequently Asked

What is money dysmorphia, in one sentence?

A persistent gap between your actual financial reality and your felt sense of it — feeling broke when you're objectively comfortable, or feeling fine when the numbers don't support it. Not a clinical diagnosis; a useful name for something that was happening anyway.

Is money dysmorphia worse for one income bracket than another?

Counter-intuitively, it shows up most clearly in higher-earning households, because the visible disconnect is bigger. Someone making $30,000 who feels broke is responding partly to reality. Someone making $200,000 who feels broke is the case study. Lower-income partners can absolutely have it too, but it's harder to separate from genuine pressure.

How do I bring this up with my partner without sounding like I'm diagnosing them?

Lead with yourself. "I think I might do this thing where I feel broke even when we're fine — can I tell you what I noticed about myself?" is a much better entry than "I think you have money dysmorphia." Once you've modelled the vulnerability, your partner can decide whether to meet you there. Don't push if they don't.

Is this just an American problem?

The term is American, the surveys are American, but the pattern isn't. Couples in the UK, Singapore, Hong Kong, and Australia have all been describing roughly the same shape of disagreement under different names for years; the term just gives the experience a flag. We've written more about how money customs vary across cultures in the dating context — the underlying nervous-system gap shows up everywhere.

Should we merge our finances or not?

This article is firmly not financial advice. What we will say: couples with money dysmorphia in the mix sometimes do worse with fully merged finances, because the dysmorphic partner can't see "their own" money clearly. A common-ground arrangement — joint account for shared expenses, separate accounts for personal spending — gives both partners a sense of agency without forcing the merge. But this is a conversation, not a rule.

The hopeful thing about money dysmorphia in relationships is that it's a name. Things with names are easier to talk about than things without them. Once "I think we have a money dysmorphia situation" is something you can both say out loud — instead of you're being unreasonable versus you don't take this seriously — you stop being adversaries and start being two people looking at the same problem from inside two different nervous systems. Which is closer to the truth than either of you was getting to alone.

Want a structured way to start the money conversation? Heart to Heart hands you 195 questions designed for exactly this kind of talk — including the earliest-money-memory prompt above. Browser-based, no accounts. The structure does the asking so you don't have to. It's part of Unravel: Couple Games, a small collection of offline games for two.

Try Heart to Heart